Welcome to our Winter edition of On the Marc. This edition will review markets for the final quarter of the 2022 financial year and consider the outlook for the foreseeable future.

Market update

Growing recession fears triggered a sharp selloff over the quarter, with the correction accelerating noticeably in the latter stages of June. Inflation data continues to come in above expectations, leading to a more aggressive policy response from central banks around the world. During the month of June alone, the Bank of England increased interest rates by 25bps, the Reserve Bank of Australia by 50bps, and the Federal Reserve by 75bps. With central bankers doubling down in their fight against inflation, interest rate increases are occurring at the same time that economic data and commentary from corporates suggest a broader slowdown is afoot.

The Australian share market closed out the financial year with the S&P/ASX 200 falling sharply by -8.8% in June. Ten out of eleven sectors finishing lower. Specifically, the Consumer Staples sector was the only positive finisher for the month (+0.2%). The Materials (-12.4%) and Financials ex-Property (-11.8%) sectors were the biggest laggards as recessionary fears weighed down risk assets across various sectors.

Australia's official unemployment rate has dropped to 3.5%, with an estimated 88,400 jobs added to the economy last month. This is a steep fall from the 3.9% unemployment rate seen for the previous three months, and sets a fresh record low jobless rate since the Australian Bureau of Statistics (ABS) jobs numbers became monthly in 1978.

Global equities were down in June (-4.5%) with healthcare, consumer staples and utilities outperforming whilst materials, energy and information technology underperformed. US equities were down (-4.4%) with headline inflation higher than expected, resulting in the Federal Reserve hiking the funds rate by 75bps, rather than the anticipated 50bps. With macroeconomic data showing signs of an economic slowdown, fears of a hard landing and deeper recession intensified. European equities underperformed broader global markets over the month (-6.1%) with fears of an energy crisis lead recession intensifying in the event of Russia reducing the flow of natural gas into the region. With European inflation data coming in stronger than expected, the ECB reiterated its hawkish tone while introducing supportive measures for sovereign periphery yields. The Bank of England hiked rates again, with the Swiss Reserve Bank and Norwegian central bank, Norges Bank, both hiking rates above market expectation.

New global COVID cases continue to rise in July, as the more transmissible (but no more harmful) Omicron BA4 and BA5 subvariants come to dominate. The rise is being led by Europe, but with South America, the US, Japan, Australia and New Zealand also seeing an increases in cases.

While eligibility for a fourth vaccine dose has now been widened in Australia to those aged over 30, a concern is that third shots (i.e. the first booster) – which are important in protecting against serious illness from Omicron - appear to have stalled out at around 54% of the population. Australia remains behind many other developed countries in the proportion of the population with third vaccination.

Fortunately, South Africa’s experience with Omicron BA4 and BA5 in April/May augur well in that it saw a brief spike in new cases, but hospitalisations and deaths remained subdued. So, while the latest wave combined with the flu and winter risks increased worker absence, another significant economic disruption in Australia from COVID similar to those seen prior to Omicron is hopefully unlikely. Some restrictions - like mask mandates and maybe even work from home advice - are likely to return though in order to keep pressure off hospitals.

The news on the Federal budget deficit remains positive. While high inflation and rising interest rates are putting pressure on the new Government to cut spending to reduce the budget deficit (and this is likely to be evident in the October Budget), a surge in corporate tax revenue (associated with high commodity prices), rising personal tax collections (due to strong jobs growth) and reduced unemployment benefit payments continue to put pressure on the budget deficit downwards. For the financial year to May, the deficit is $27bn less than projected in the March Budget. This implies that the budget deficit for 2021-22 will come in at around $45-50bn, well below the $80bn projected in March.

Economic recoveries never go in a straight line, but it’s clear that this one will be very bumpy, as coronavirus continues to rear its ugly head and as the reverberations on businesses, jobs and households continue well into the future. Economists expect the Deep 'V' rebound reflected in recent data to give way to a slower, bumpier recovery going forward. In saying this, the share market and the economy don't necessarily move in tandem as illustrated coming out of the Global Financial Crisis (GFC) wherein 2009 the share market started the longest bull market in history.

Major global economic events

The US non-manufacturing ISM index rose sharply in June, jobless claims continued to fall, and job openings and hiring rose in May. The labour market is still very weak, and as noted earlier, more recent economic data indicates some faltering lately, with the resurgence in new coronavirus cases.

Eurozone retail sales rebounded by a stronger than expected 17.8% in May, but the recovery in German factory orders and industrial production was less than expected.

Japanese household spending and wages fell more than expected in May, but the Economy Watchers household and business sentiment indicators rose more than expected in June.

Chinese inflation remained weak in June, indicating that there is no constraint on further stimulus from the People’s Bank of China (PBOC). CPI inflation edged up to 2.5% year-on-year due to higher food price inflation, but core inflation fell to just 0.9%. Meanwhile, total credit was stronger than expected in June, accelerating to 12.8% year-on-year.

Market returns for major indices

Below is a table showing the percentage returns of the major market indices to 30th June 2022.

Source: Bloomberg

The outlook for the year ahead

Market expectations for rate hikes have generally fallen over the last three weeks as inflation fears have receded a bit and economic data has slowed. For example, the market’s expectation of the Fed Funds rate at year-end has fallen from 3.7% three weeks ago to 3.47% now, while the market’s expectation for the RBA’s cash rate at year-end has fallen from 3.86% three weeks ago to 3.14%. The hawkish pivot a month or so ago by central banks, including the RBA, has seen market expectations for longer-term inflation fall. What’s more, various indicators suggest that inflation pressures in the US may have peaked and if so, this is a positive sign for other countries, including Australia, as the US is leading other countries by about six months in inflation.

On a 12-month view, we remain optimistic that shares can rise on the grounds that cooling inflation pressures, as suggested by our Pipeline Inflation Indicator, should enable central banks to ease up on the interest rate brake in time to avoid a recession (or at least avoid a deep recession). With US inflation pressures slowing, it’s unlikely that the Fed needs to cause a recession to get inflation under control. While the 10-year yield less 2- year yield US yield curve has inverted, the 10-year less Fed Funds rate yield curve, which has inverted prior to all US recessions since 1970, is yet to invert. In Australia, the various yield curves are still far from inverting (not that they have been a great guide). An inverted yield curve occurs when the long-dated bonds trade at a lower yield than the shorter-dated bonds. For example, the 10-year yield is 3% whereas the 2-year trades at 2%.

The latest NSW floods are devastating for those directly impacted but are more inflationary than deflationary and so are unlikely to see the RBA change course. Analysing the economic impact of the latest floods is complicated because it is now the fourth major flood this year for some areas. While they will cause short-term disruption to economic activity the net effect as with most natural disasters is likely to be stimulatory as rebuilding kicks in (yet again). On a six-month horizon, the recent floods are more likely to add to economic growth rather than detract from it. They will add to inflationary pressure because of further disruption to fruit and vegetable supplies and increased demand for household furnishings and other equipment, building materials, and workers in short supply.

The Australian Dollar is likely to remain volatile in the short term as global uncertainties persist. However, a rising trend is likely over the next 12 months as commodity prices ultimately remain in a super cycle bull market.

The US may be edging towards cutting some of its Trump-era China tariffs and passing a shrunken Build Back Better budget reconciliation package – but both may have little macro impact. The Trump tariffs imposed on $360bn of China imports disrupted US economic activity but didn’t add much too measured inflation, so the removal of tariffs on a proposed $10bn of goods won’t have much impact in cutting inflation either. If a reconciliation package is passed, it will be a fraction of the size proposed last year, which is why it’s often called Build Back Smaller. If tax increases proceed on high-income earners, capital gains and dividends then it may have more impact on investment markets, but this looks to have been replaced with a surtax on very-high income earners (amounting to just 17,000 taxpayers), and even this looks to have been dropped.

Did you know?

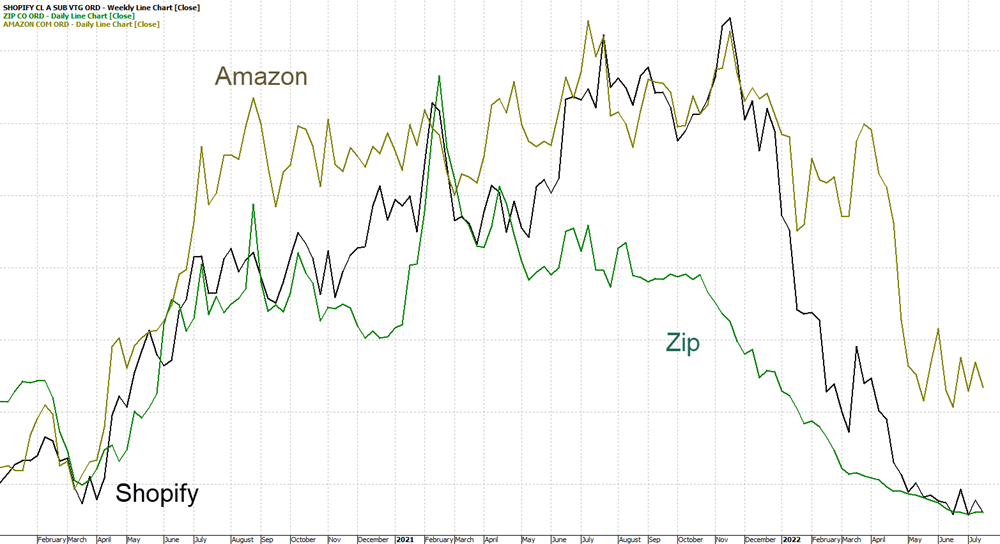

Most of the shares that experienced the largest gains during the first 18 months of Covid are back to where they were (or lower) than before Covid. The following chart shows the share price of Amazon, Shopify and Zip (afterpay’s main domestic competitor ) from January 2020 through to now. The large increase was due to valuations based on interest rates staying close to zero and significant online buying of discretionary items continuing forever. Both of these expectations from some investors were not realistic. In February last year, Zip reached an all-time high of $14.53. Today it is trading at $0.53.

Final reMarc

Shares are likely to see continued short term volatility as central banks continue to tighten to combat high inflation, the war in Ukraine continues and fears of recession remain high. However, we see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year, allowing central banks to ease up on the monetary policy brakes.

We are in unprecedented times however have confidence that by investing in funds that own companies that make money (billions), their profit is expected to increase into the future and have low levels of debt that over time a fruitful outcome will be achieved.

"The bad news is time flies. The good news is you're the pilot."

Michael Altshuler

Key Facts & Figures

1. Australian Cash Rate has increased in three months from the record low of 0.1% to 1.35%.

2. The RBA Cash Rate is poised to increase (79% probability) a further 0.50% in August to 1.85%.

3. Our annualised inflation rate is 5.1%. This is above the upper end of the RBA’s target band of 2 - 3%.

4. Australia’s unemployment rate is 3.5%.

5. The Federal Reserve cash rate has risen from the record low and currently is between 1.5% and 1.75% in the US. The Federal Reserve cash rate forecast is to be above 3.5% by the end of 2022. Only three months ago, the year-end forecast was 1.90%.