Welcome to the Summer edition of On the Marc. In this edition, we will review markets for the final quarter of 2025 and consider the outlook for the foreseeable future.

Market update

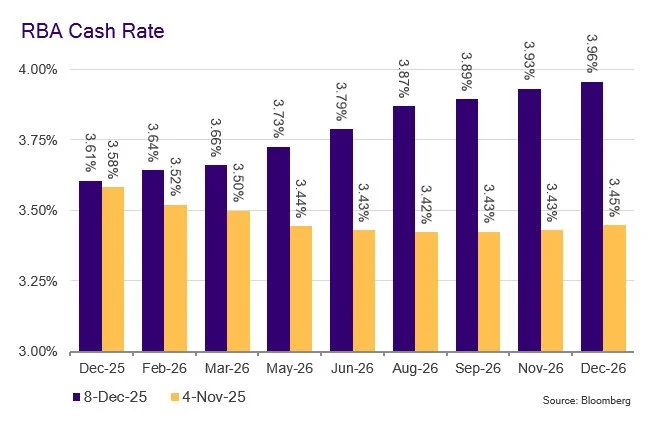

The Australian market lagged global markets in the December quarter, with the ASX200 Accumulation Index declining 1.0%. Domestic economic growth remained stable, but relatively subdued, with Gross Domestic Product (GDP) growth of only 0.4% for the September quarter. Meanwhile, CPI releases indicated a concerning step-up in inflation to levels above the RBA’s 2-3% target range, leading to a repricing of interest rate expectations. Figure 1 below shows the change in interest rate outlook for Australians in just one month (November to December).

Figure 1: Outlook for Australian Interest Rates

Source: Bloomberg

The strong performance of Resources stocks during the quarter helped offset declines across all other sectors. Materials (+13.0%), Energy (+1.2%) and Industrials (+0.1%) were the strongest contributors to the Australian share market, while Information Technology (-26.0%), Consumer Discretionary (-11.7%) and Healthcare (-9.9%) detracted.

Over the 2025 calendar year, the ASX200AI delivered a solid return of 10.3%.

Global equity markets moved modestly higher during the quarter. The USA S&P500 was up 2.7%, driven by ongoing Fed easing, strong USA economic growth, and solid corporate earnings growth. While the USA GDP growth increased to 4.3% in Q3, unemployment also crept up to 4.6% for November 2025. This ongoing softening of the USA labour market led the Fed to cut rates by 25 basis points (bps) at both FOMC meetings in the quarter.

These developments have widened the divergence in monetary policy and interest rate expectations between the USA and Australia. Markets currently expect a further two 25bps rate cuts in the USA in 2026, while at the same time pricing in at least one rate hike in the Australian market – a backdrop that increasingly favours Australian Dollar strength.

The gold price continued to rally, up a further 12% for the quarter. This continues to be driven by large and growing US federal fiscal deficits and debt levels, US dollar devaluation, emerging-market central bank buying, and a global interest rate-cutting cycle.

In the USA, S&P 500 companies reported strong earnings growth of approximately 14% in 2025. Corporate earnings were also robust, with more than 80% of S&P 500 companies reporting Q3 2025 earnings above consensus expectations. Inflation eased modestly relative to market expectations, with core CPI declining to 2.6% in November and December. On the negative side, labour markets continued to soften, with the unemployment rate rising to 4.6% in November, from 4.0% at the end of 2024, driven primarily by a decline in Federal Government employment.

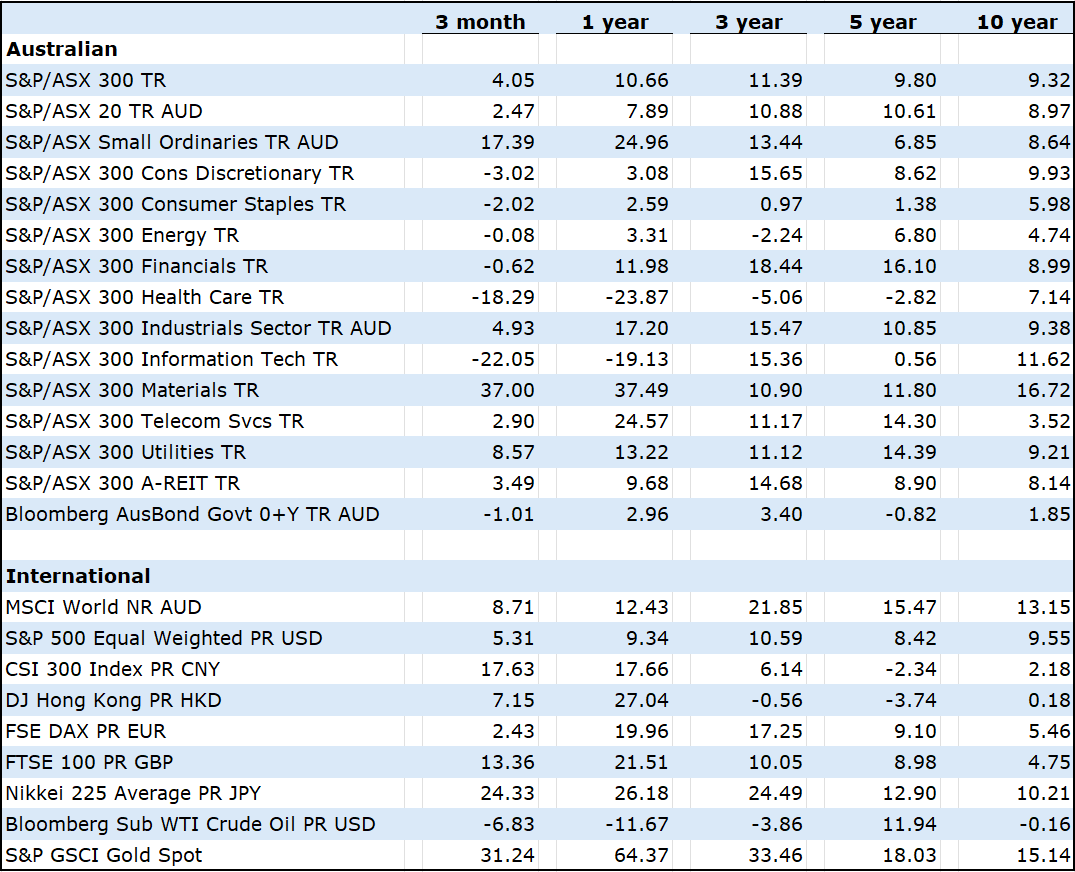

Market returns for major indices

Below is a table showing the percentage returns of the major market indices to 31st December 2025.

Source: Morningstar

The outlook for the year ahead

Equity markets enter 2026 at an inflection point, shaped by several powerful factors that will likely influence returns, including divergent interest rate paths domestically and offshore, artificial intelligence, global geopolitics, and a resources complex that may be in the early innings of a boom.

A defining macroeconomic feature of 2026 will be the asynchronous monetary-policy cycle between Australia and major offshore economies. Australia’s inflation profile has proven stickier than peers', forcing the RBA into a hawkish pivot and prompting many commentators to expect interest rate hikes in 2026. While in Australia, economic growth is accelerating, and consumption remains resilient, persistently weak productivity is creating an inflationary pulse and raising interest rate expectations. This contrasts with many other global economies that are moving more aggressively towards easing, particularly the US, which is exhibiting both strong growth and disinflation courtesy of a productivity boom. This divergence has important implications for relative valuations, with higher rates in Australia placing downward pressure on fair multiples, currency (stronger AUD) and sector leadership, with the US likely to enjoy a broadening out of the equity rally and Australia likely to favour late-cycle exposures, such as Resources and Consumer Staples.

Political developments, both internationally and in key domestic markets, remain a wildcard. The Liberation Day tariff policy created massive market uncertainty. Subsequently, policies have been watered down, deals done, exceptions made, and timeframes extended.

Did you know?

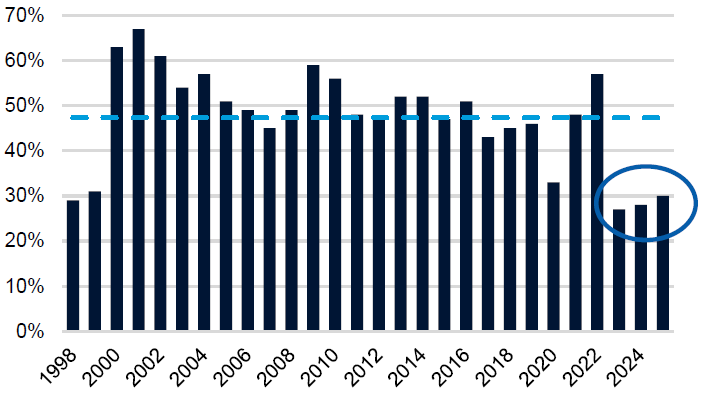

In the USA, 2025 was the third year in a row of abnormally concentrated market returns. In 2025, only 30% of the S&P 500 Index members outperformed the Index. This is similar to both 2024 and 2023, and well down on the long-term average of around 50%. Figure 2 below illustrates that, in recent years, the USA share market returns have been highly concentrated, with less than a third of companies outperforming the overall market return. This means these companies’ share prices have risen significantly, while the remaining majority of companies have been mundane.

Figure 2: S&P500 Index members outperforming the Index

Source: Bloomberg

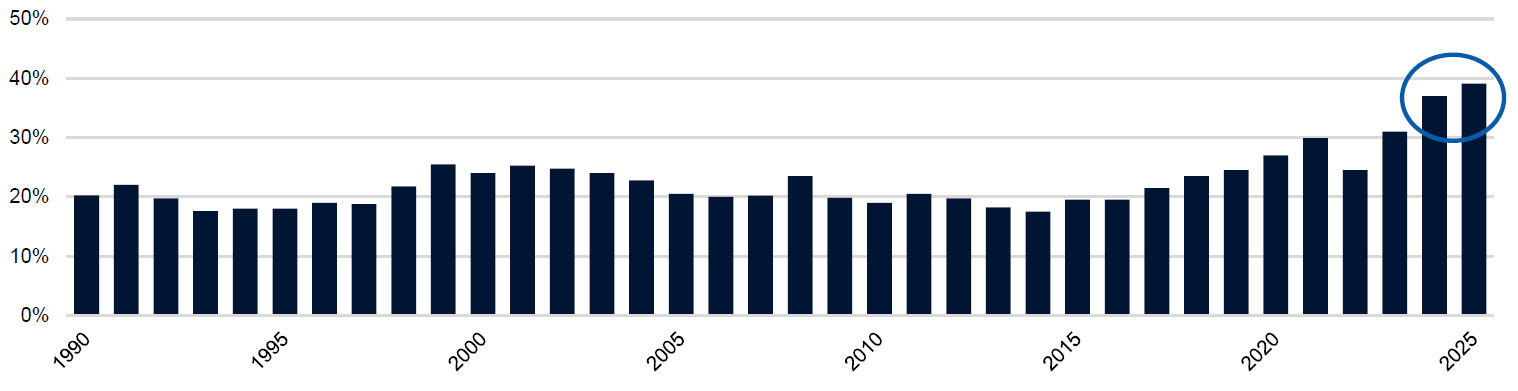

This has led to the biggest companies becoming proportionally larger, thereby making up a much greater proportion of the index than in the past 45 years. This is illustrated in Figure 3 below.

Figure 3: Weighting of top 10 S&P500 Index members

Source: S&P Dow Jones, FactSet

Final reMarc

There is a lot going on in the world at present, with geopolitical tensions high, primarily due to an unorthodox leader in the USA, President Trump. When looking back in time, there is always a lot going on; however, at present, it seems elevated. This is expected to continue throughout 2026. The financial markets seem to have accepted the elevated uncertainty in its stride, resulting in a positive outlook for equities and property this year. Along the way, no doubt, there will be decent pullbacks; however, looking at the bigger picture, it is reasonable to expect modest returns. It is pleasing that WealthMarc’s client portfolios have performed strongly in 2025 despite allocating away from index funds. We expect this to continue in 2026 (and beyond).

" Software is eating the world, but AI is going to eat software. "

Jensen Huang

Key Facts & Figures

Australian Cash Rate was on hold at the December meeting at 3.60%.

The RBA Cash Rate is likely to remain on hold in February when the RBA next meet (25% chance of an increase).

Our annualised inflation rate is 3.4%. This is above the RBA’s target band of 2 - 3%.

Australia’s unemployment rate is 4.3%.

The US Federal Reserve cash rate band is 3.50% - 3.75%.