Welcome to the Autumn edition of On the Marc. In this edition, we will review markets for the first quarter of 2026 and consider the outlook for the foreseeable future.

Market update

What a first quarter it has been! Equities initially performed well in January and February, driven by strong commodity prices (despite a more hawkish interest rate outlook). Global markets, including in Australia, then fell sharply in March following the start of the war in Iran. The sell-off was extremely broad-based in the month, other than select defensive names and energy-related stocks.

Reflecting that, Australian share market sector performance dispersion was extreme, with Energy (+34.9%), Utilities (+8.5%) and Consumer Staples (+8.1%) the strongest performers, while Information Technology (-27.9%), Healthcare (-16.9%) and Property (-17.1%) were the hardest hit.

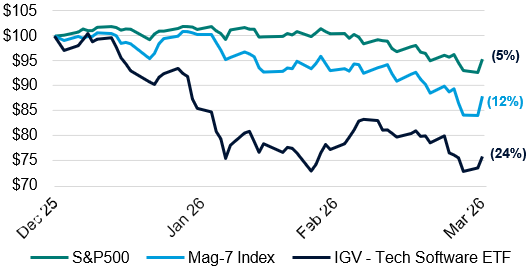

The U.S. equity market underperformed the Australian and most other markets during the quarter, with the S&P 500 declining by 4.3% (the ASX 200 was down 1.6%). The release of more advanced artificial intelligence (AI) tools in February highlighted the potential impact of AI on software industry incumbents and led to a sharp deterioration in sentiment towards these stocks, which are more prominent in U.S. indices than elsewhere.

Figure 1: US Software Shares v Mag-7 v S&P500 share price performance (March quarter)

Source: Bloomberg

The magnitude of the oil shock in March has heightened global stagflation risks and led to a sharp rise in bond yields across markets. In Australia, the RBA raised rates twice during the quarter (before the war) to respond to stubborn inflationary pressures, with markets pricing in another two hikes by the end of 2026. The U.S. Fed left rates unchanged at both of its meetings during the quarter. Bond markets are now expecting no further easing in the U.S. in 2026 after previously pricing at least two additional cuts.

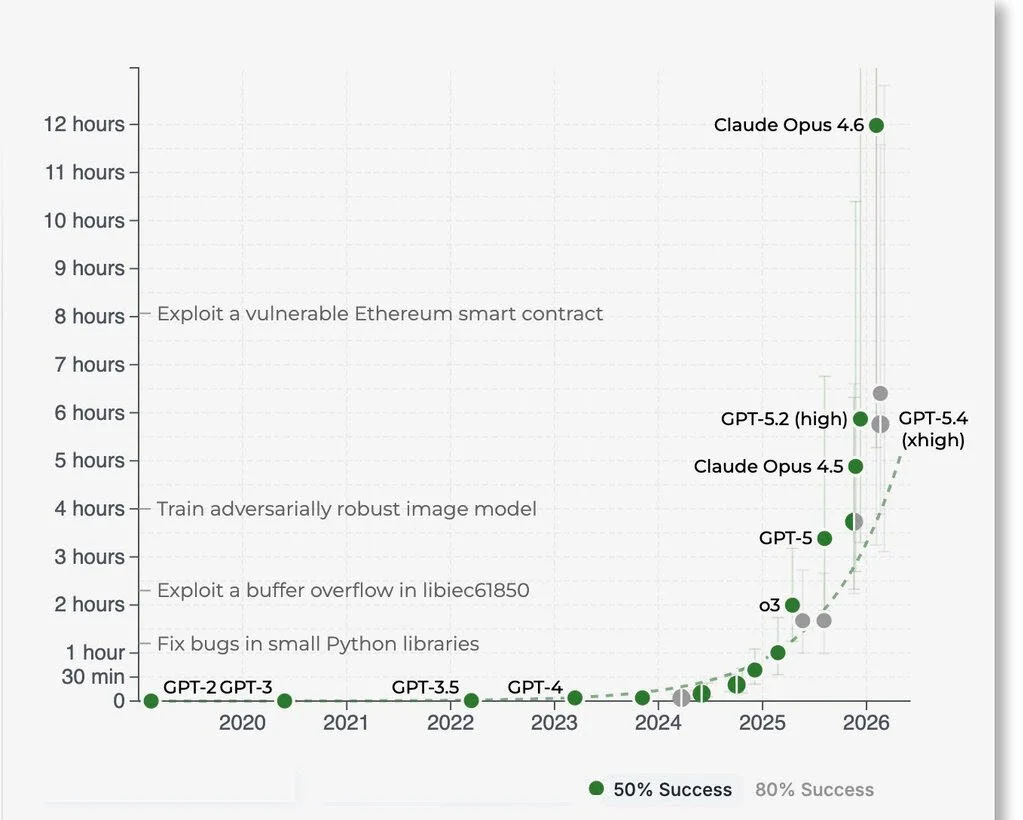

While AI itself is not new, the release of more advanced enterprise AI agents from Anthropic highlighted the potential for these systems to automate complex workflows. This suggested structural change in the tech sector could unfold in a more comprehensive manner and much more quickly than expected. This drove a structural shift in market expectations for long-term returns for some software companies, where the market had assumed extremely high revenue and earnings growth rates to continue for years to come. Figure 2 below shows the evolution of AI from a task completer to an agent. In a matter of seconds, models can complete complex tasks that would take many hours for a human.

Figure 2: Evolution of AI in Replacing Human Hours to Complete a Task

Source: Model Evaluation and Threat Research, April 2026

Market returns for major indices

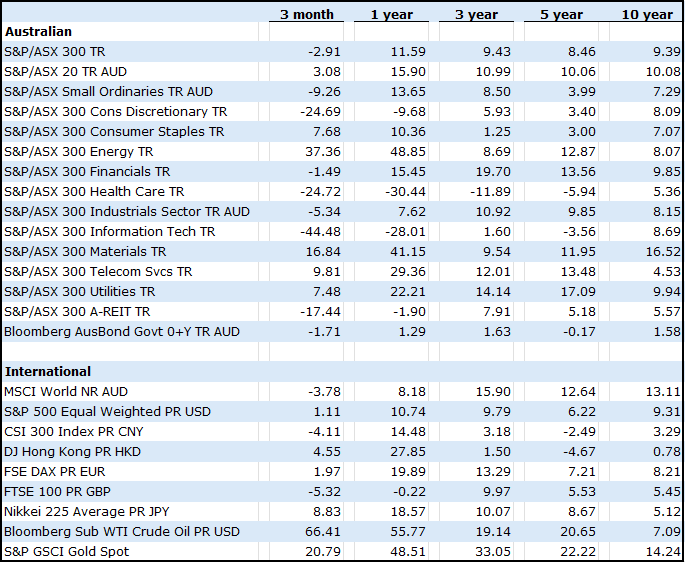

Below is a table showing the percentage returns of the major market indices to 31st March 2026.

Source: Morningstar

The outlook for the year ahead

Looking ahead to the remainder of 2026, markets are likely to be driven in the near term by political developments in the Middle East. If the conflict is resolved over the coming weeks, markets may be able to look through what would likely be a transitory inflation shock. In this scenario, investor focus is likely to return to the more constructive backdrop that was in place prior to the escalation in tensions. If the conflict is not resolved in the near term, particularly if oil supply remains disrupted through the Strait of Hormuz, the outlook becomes materially more challenging. A sustained increase in global oil prices has historically been a very reliable indicator of recession risk. In fact, a sustained rise of 50% or more in oil prices for periods longer than 12 months has preceded nine of the past ten U.S. recessions since World War II. It is important to note that the United States has significantly increased its domestic oil production over recent years, making it less exposed to supply-driven oil shocks than in the past. That said, it remains unlikely that the U.S. would be able to fully insulate itself from the broader repercussions of a global recession should one emerge.

If the conflict is resolved in the short term, fixed income yields may retreat (the chance of future interest rate rises diminishes). Even here, however, there is uncertainty about how much economic damage has already been done, particularly regarding inflation. A longer lasting conflict would be more concerning and would likely place upward pressure on yields. Either way, yields have moved higher once again from an already elevated base, which continues to provide attractive income opportunities for investors.

Equity markets have experienced significant dispersion in performance. We continue to believe that the artificial intelligence theme is structural in nature, and short term market volatility is unlikely to undermine this longer term opportunity. Prior to the conflict, equity markets appeared to be in a good place with strong earnings, and a resolution would likely support a return to more positive sentiment.

Given this environment, it is difficult to predict how the remainder of the year will unfold across asset classes, as outcomes remain heavily dependent on an inherently unpredictable factor: the trajectory of the Iran conflict. At the time of writing, the U.S. share market is at an all time high, and the Australian share market is within 5% of an all time high. This indicates that the market is pricing in the Iran conflict as close to a permanent resolution.

Did you know?

Data suggests that human happiness follows a "U-curve," typically bottoming out in our 40s and early 50s before climbing significantly as we enter our 60s and 70s.

Retirement isn’t just about stopping work; for many, it’s statistically the most content period of their lives. We aren't just planning for "old age"—we’re planning for your "happiness peak".

Final reMarc

There is a lot to be concerned about at present; however, the media fixates on negative news, and it is at such times that we need to take a step back and look at the bigger picture. That is, over time, growth assets outperform defensive assets by a significant amount. Through events such as COVID-19, the Russia–Ukraine war, major policy shifts, and now the Iran conflict, we are painted a picture of financial Armageddon. However, historically, the share market has always gone on to make all time highs (as profitable companies grow and hence gross domestic product expands), and when looking back at these major world events, they do not seem as significant through a financial lens. Time in the market achieves rewarding long term outcomes for clients that remain invested regardless of short term headlines. When looking at the world through a pragmatic lens, it is hard to fathom that with Trump’s erratic and unpredictable nature, along with the world’s oil supply heavily constrained, the markets are at or near all time highs. But this is the world we live in!

" The stock market is a device for transferring money from the impatient to the patient. "

Warren Buffett

Key Facts & Figures

Australian Cash Rate increased by 0.25% at the March meeting to 4.10%.

The RBA Cash Rate is likely to increase in May, when the RBA next meets (a 62% chance of an increase).

Our annualised inflation rate is 3.7%. This is above the RBA’s target band of 2 - 3%.

Australia’s unemployment rate remains steady at 4.3%.

The US Federal Reserve cash rate band is 3.50% - 3.75%.